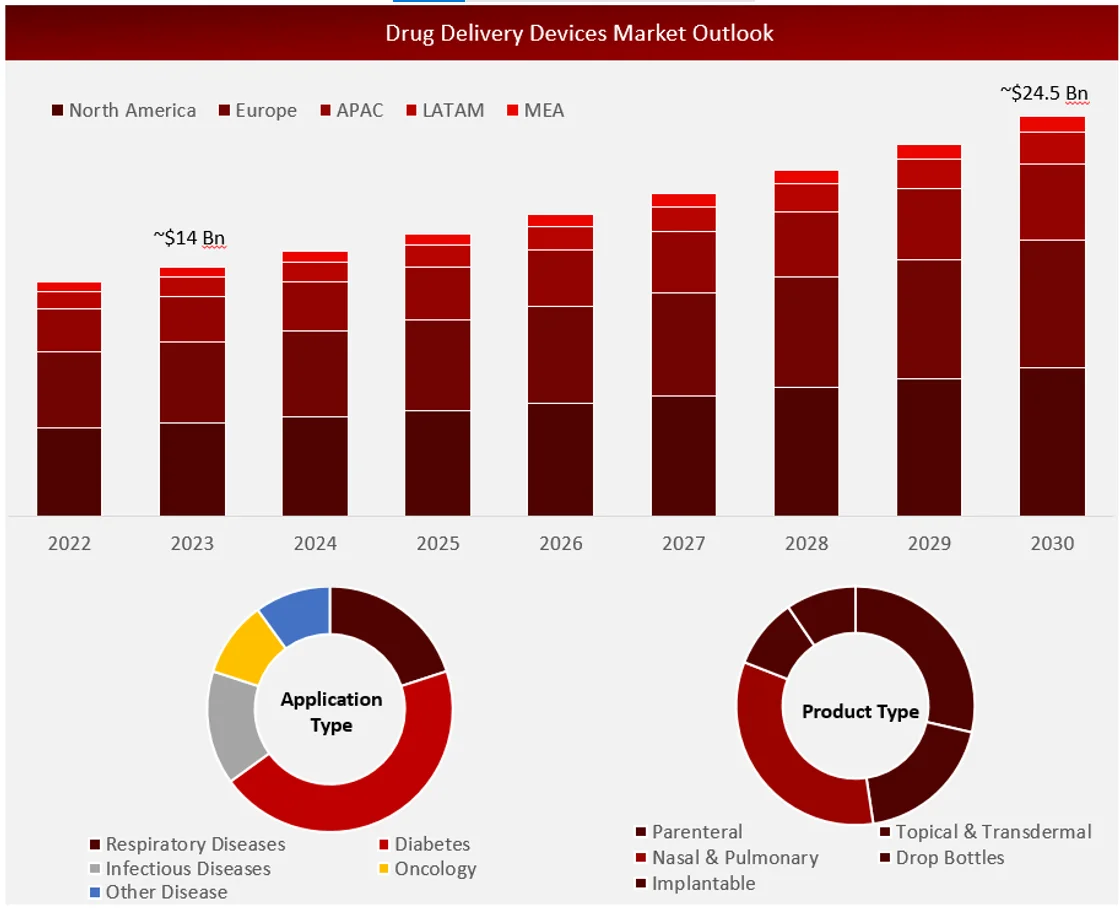

Wissen Research analyses that the global drug delivery device market is estimated at ~USD 14 billion in 2023 and is projected to reach ~USD 24 billion by 2030, expected to grow at a CAGR of ~7.5% during the forecast period, 2023-2030.

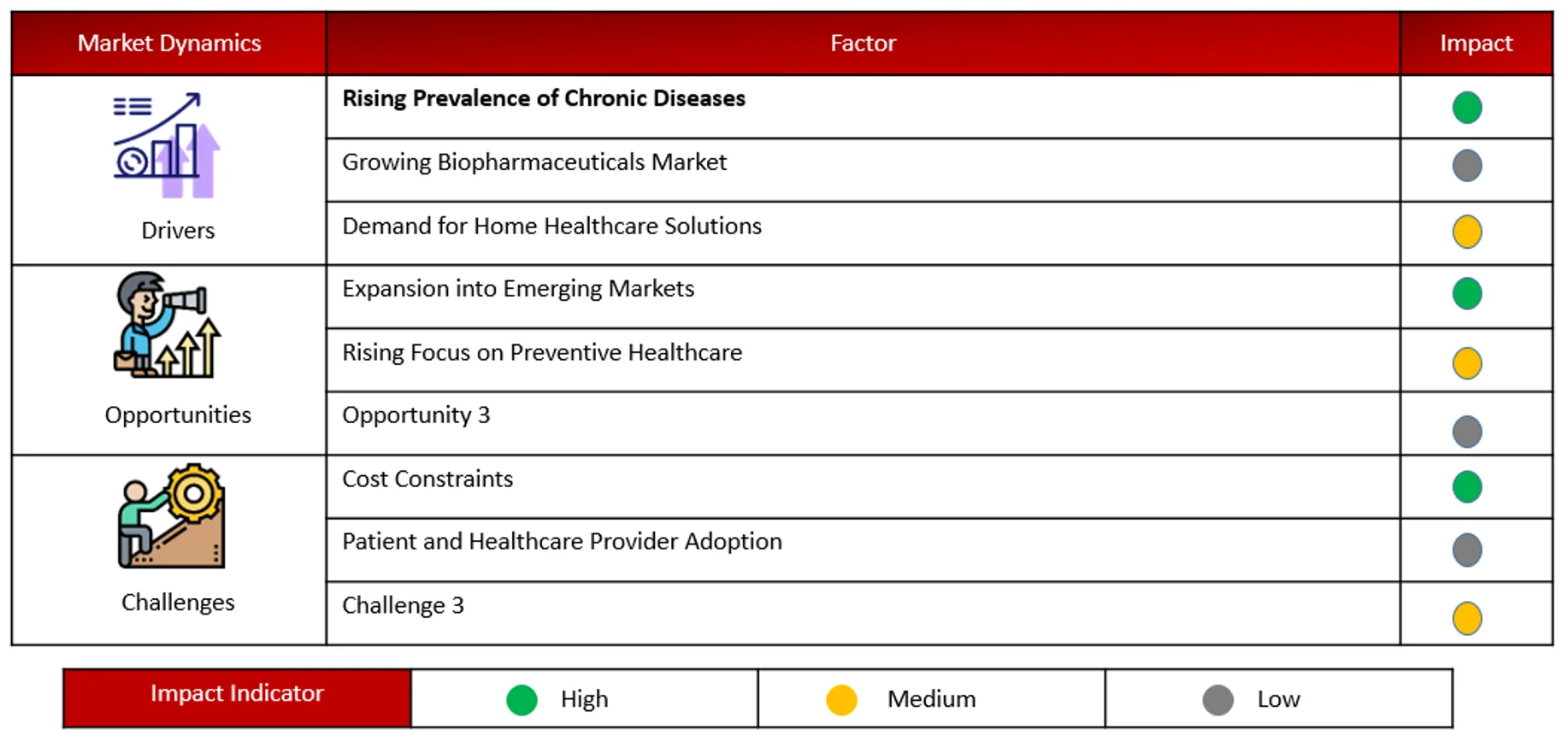

The drug delivery market is rapidly expanding due to advancements in technology, such as nanotechnology and smart delivery systems, which enhance precision and effectiveness. The rising prevalence of chronic diseases and the growth of the biopharmaceutical sector drive demand for specialized and targeted drug delivery solutions. Additionally, an aging population and expanding healthcare access in emerging markets contribute to the market’s growth. Increased focus on patient compliance and supportive regulatory and investment environments further accelerate innovation in this sector.

Driving Factor: Rising Prevalence of Diseases

The rising global incidence of acute and chronic diseases, including infections, is a key driver of market growth. For example, a recent report highlights that over 20 million people in the country currently have diabetes, with projections indicating this number will exceed 57 million by 2025. This significant increase is expected to further propel the market, contributing to the expansion of the drug delivery devices sector within the projected timeframe.

Opportunity: Rising Public and Private Investment in Targeted Research Initiatives

The increase in public and private funding for targeted research, coupled with rising air pollution levels and continuous technological advancements driving product innovations, is expected to create lucrative opportunities for market players from 2023 to 2030. Additionally, the growing number of strategic partnerships, expanding internet connectivity, increasing healthcare facilities, and higher per capita healthcare expenditure will further boost market growth during this period, offering further profit potential for industry participants.

Challenge: High Costs Linked to Research and Development Activities

High costs associated with research and development, limited infrastructure, and stringent regulations on drug delivery systems are anticipated to hinder market growth. Additionally, challenges such as inadequate reimbursement scenarios, slow technology adoption in developing economies, availability of low-cost alternatives, and insufficient infrastructure in low- and middle-income countries are expected to impact the market from 2023 to 2030.

This drug delivery devices market report details recent developments, trade regulations, import-export analysis, production assessments, value chain optimization, market share insights, and the influence of both domestic and international market players. It also covers emerging revenue opportunities, changes in market regulations, strategic growth analyses, market size, category growth, application niches, product approvals, launches, geographic expansions, and technological innovations. For more information on the drug delivery devices market, contact Data Bridge Market Research for an Analyst Brief, and our team will assist you in making informed decisions to achieve market growth.

Diabetes Drug Delivery Devices Dominate Market in Drug Delivery Device by Application

In 2023, drug delivery devices for diabetes led the market with the highest share, primarily due to the rising prevalence of diabetes. These devices are leading the market due to their essential role in managing blood glucose levels for millions of diabetics. Innovations such as insulin pumps, continuous glucose monitors, and smart insulin pens are driving growth by providing more precise, convenient, and effective management of diabetes compared to traditional methods. This dominance is driven by the increasing prevalence of diabetes and ongoing advancements in technology that enhance patient compliance and treatment outcomes. .

North America to hold the largest share in the Drug Delivery Device Market

North America leads the drug delivery devices market due to its robust healthcare infrastructure, increasing investments from major players in advanced device development, a growing number of drug development processes, and a high prevalence of chronic diseases. The region also benefits from the presence of numerous pharmaceutical companies and a rise in research activities.

Major Companies and Market Share Insights in Drug Delivery device market

Major players operating in drug delivery device market are Koninklijke Philips, Novartis AG, Gerresheimer AG, Omron Corporation, Gemini Pharmaceuticals, GMP Laboratories of America, Becton, Dickinson and Company, West Pharmaceutical Services, Inc., Bright Pharma Caps, Recipharm AB, Resyca GmBH among others.

Recent Developments in Drug Delivery Device Market:

Introduction

Market Definition

Drug delivery devices are medical tools or systems engineered to administer medications or therapeutic substances to patients. These devices are created to enable the delivery of drugs in various forms, including injections, inhalation, transdermal patches, implants, and oral routes. The drug delivery device market does not include the formulation in the report.

Sources: Company Websites and Wissen Research Analysis.

Sources: Wissen Research Analysis.

Key Stakeholders

Key objectives of the Study

Research Methodology

The aim of the study is to examine the key market forces such as drivers, opportunities, restraints, challenges, and strategies of key leaders. To monitor company advancements such as patents granted, product launches, expansions, and collaborations of key players, analyzing their competitive landscape based on various parameters of business and product strategy. Markey sizing will be estimated using top-down and bottom-up approaches. Using market breakdown and data triangulation techniques, market sizing of segments and sub-segments will be estimated.

Sources: Wissen Research Analysis.

Research Approach

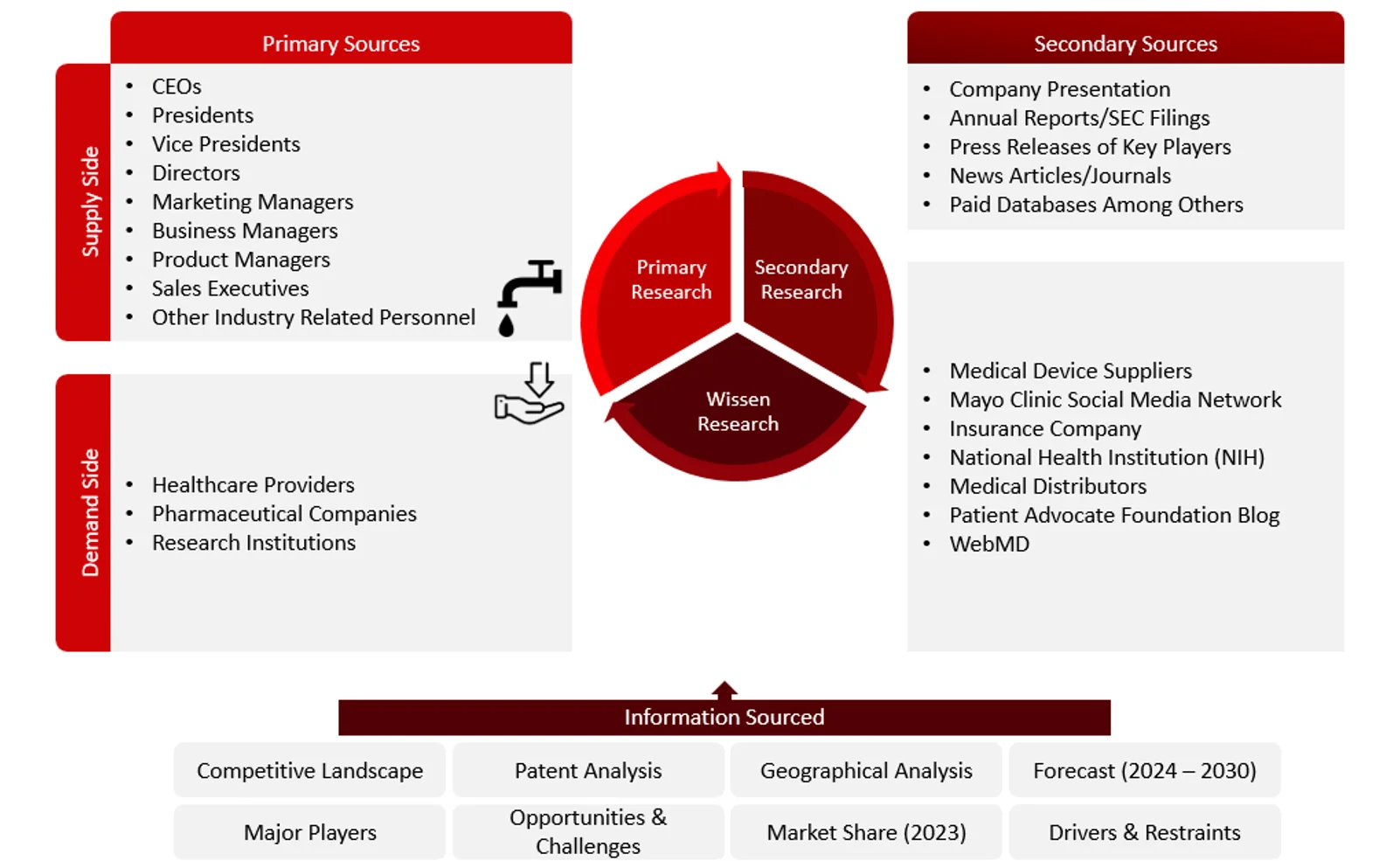

Collecting Secondary Data

The process of collating secondary research data involves the utilization of databases, secondary sources, annual reports, investor presentations, directories, and SEC filings of companies. Secondary research will be utilized to identify and gather information beneficial for the in-depth, technical, market-oriented, and commercial analysis of the drug delivery device market. A database of the key industry leaders will also be compiled using secondary research.

Collecting Primary Data

The primary research data will be conducted after acquiring knowledge about the drug delivery devices market scenario through secondary research. A significant number of primary interviews will be conducted with stakeholders from both the demand and supply side (including various industry experts, such as Vice Presidents (VPs), Chief X Officers (CXOs), Directors from business development, marketing and product development teams, product manufacturers) across major countries of Europe, Asia Pacific, North America, Latin America, and Middle East and Africa. Primary data for this report will be collected through questionnaires, emails, and telephonic interviews.

FIGURE: BREAKDOWN OF PRIMARY INTERVIEWS FROM SUPPLY SIDE

FIGURE: BREAKDOWN OF PRIMARY INTERVIEWS FROM DEMAND SIDE

FIGURE: PROPOSED PRIMARY PARTICIPANTS FROM DEMAND AND SUPPLY SIDE

Note: Above mention companies are non-exhaustive.

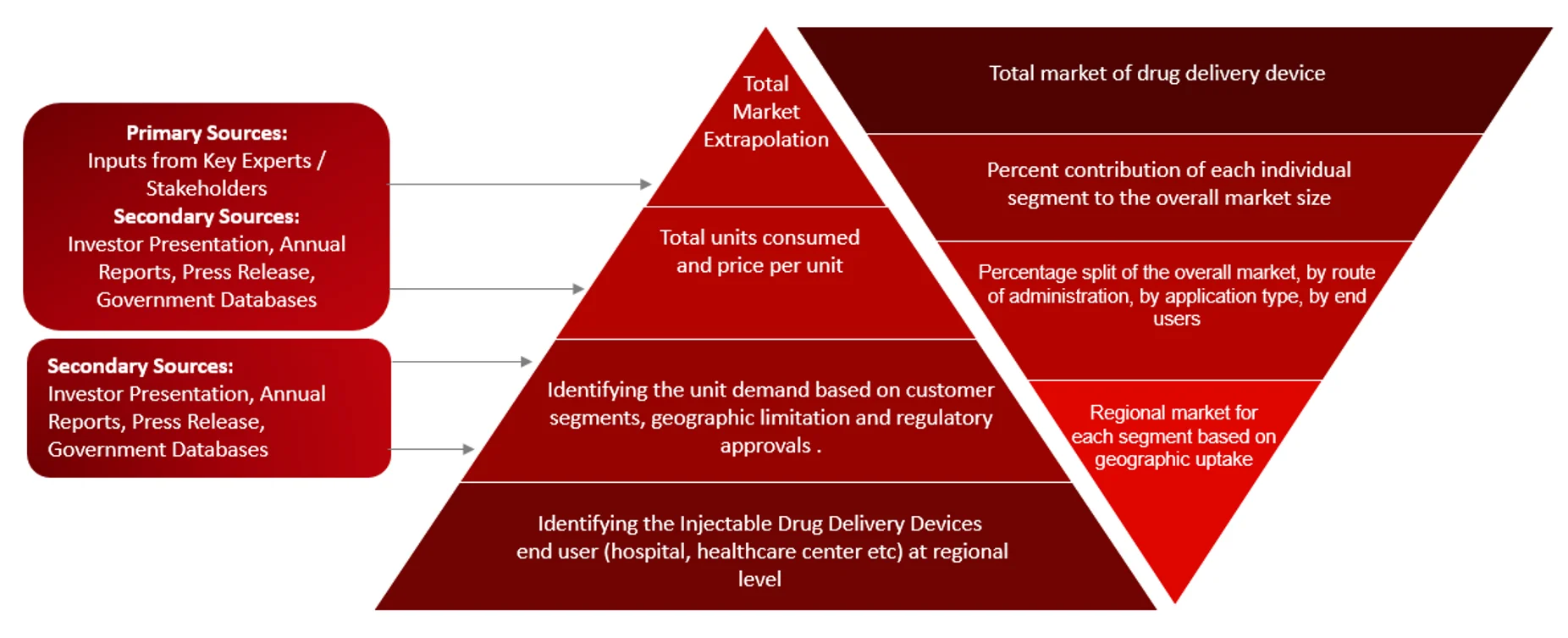

Market Size Estimation

All major manufacturers offering various drug delivery devices services will be identified at the global / regional level. Revenue mapping will be done for the major players, which will further be extrapolated to arrive at the global market value of each type of segment. The market value of drug delivery devices market will also split into various segments and sub segments at the region level based on:

FIGURE: REVENUE MAPPING BY COMPANY (ILLUSTRATION)

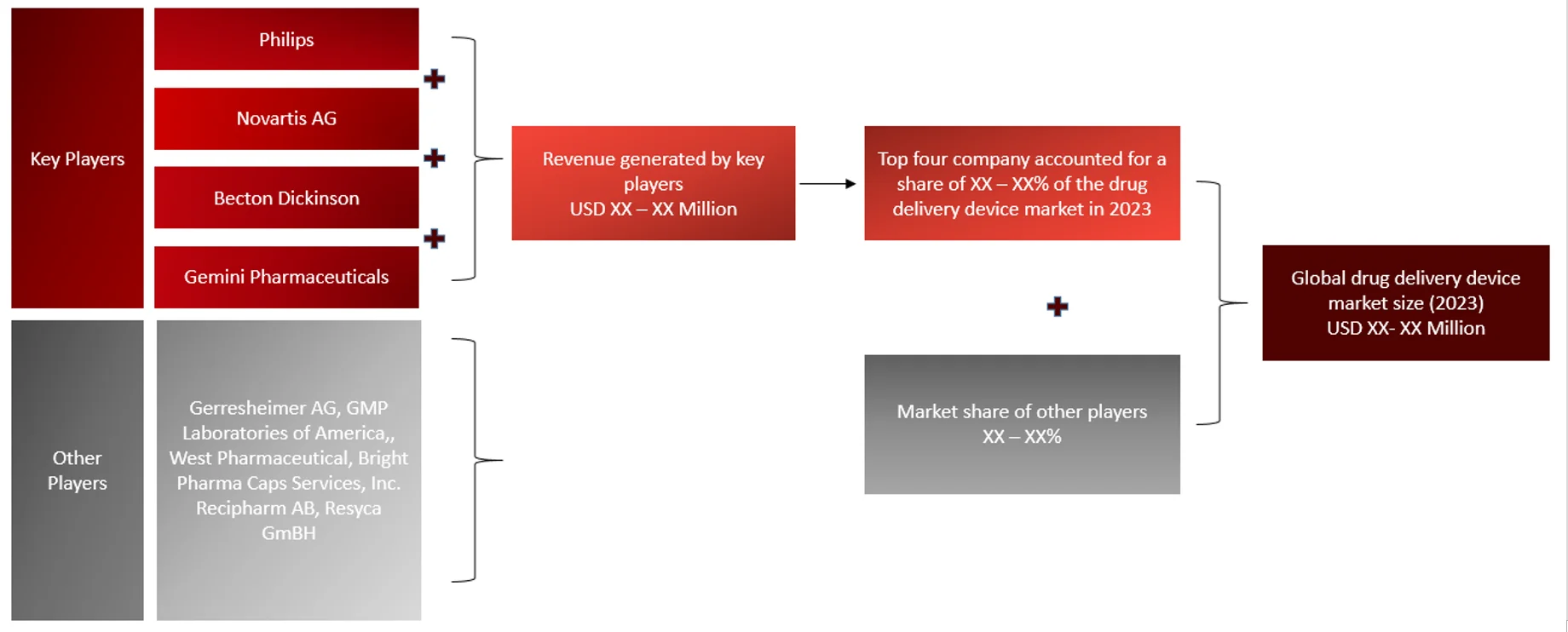

FIGURE: REVENUE SHARE ANALYSIS OF KEY PLAYERS (SUPPLY SIDE)

FIGURE: MARKET SIZE ESTIMATION TOP-DOWN AND BOTTOM-UP APPROACH

Sources: Company Websites, Annual Reports, SEC Filings, Press Releases, Investor Presentation, Paid Database, and Wissen Research Analysis.

Sources: Company Websites, Annual Reports, SEC Filings, Press Releases, Investor Presentation, Paid Database, and Wissen Research Analysis.FIGURE: ANALYSIS OF DROCS FOR GROWTH FORECAST

FIGURE: GROWTH FORECAST ANALYSIS UTILIZING MULTIPLE PARAMETERS

Sources: Company Websites, Annual Reports, SEC Filings, Press Releases, Investor Presentation, Paid Database, and Wissen Research Analysis.

Sources: Company Websites, Annual Reports, SEC Filings, Press Releases, Investor Presentation, Paid Database, and Wissen Research Analysis.Research Design

After arriving at the overall market size-using the market size estimation processes-the market will be split into several segments and sub segment. To complete the overall market engineering process and arrive at the exact statistics of each market segment and sub segment, the data triangulation, and market breakdown procedures will be employed, wherever applicable. The data will be triangulated by studying various factors and trends from both the demand and supply sides in the drug delivery device market.

1. INTRODUCTION

1.1 KEY OBJECTIVES

1.2 DEFINITIONS

1.2.1 IN SCOPE

1.2.2 OUT OF SCOPE

1.3 SCOPE OF THE REPORT

1.4 SCOPE RELATED LIMITATIONS

1.5 KEY STAKEHOLDERS

2. RESEARCH METHODOLOGY

2.1 RESEARCH APPROACH

2.2 RESEARCH METHODOLOGY / DESIGN

2.3 MARKET SIZING APPROACH

2.3.1 SECONDARY RESEARCH

2.3.3 PRIMARY RESEARCH

3. EXECUTIVE SUMMARY & PREMIUM CONTENT

3.1 GLOBAL MARKET OUTLOOK

3.2 KEY MARKET FINDINGS

4. MARKET OVERVIEW

4.1 MARKET DYNAMICS

4.1.1 DRIVERS/OPPORTUNITIES

4.1.2 RESTRAINTS/CHALLENGES

4.2 END USER PERCEPTION

4.3 NEED GAP

4.4 SUPPLY CHAIN / VALUE CHAIN ANALYSIS

4.5 INDUSTRY TRENDS

4.6 PORTER’S FIVE FORCES ANALYSIS

5. PATENT ANALYSIS

5.1. PATENTS RELATED TO DRUG DELIVERY DEVICES

5.2. PATENT LANDSCAPE AND INTELLECTUAL PROPERTY TRENDS

6. GLOBAL DRUG DELIVERY DEVICES MARKET, BY PRODUCT (2023-2030, USD MILLION)

6.1 PARENTERAL DRUG DELIVERY SYSTEMS

6.1.1 SYRINGES

6.1.1.1 CONVENTIONAL SYRINGES

6.1.1.2 PREFILLED SYRINGES

6.1.1.3 SAFETY SYRINGES

6.1.2 PEN INJECTORS

6.1.3 AUTOINJECTORS

6.1.4 WEARABLE INJECTORS/ON-BODY DRUG DELIVERY SYSTEM

6.1.5 NEEDLE FREE INJECTORS

6.2 TOPICAL & TRANSDERMAL DRUG DELIVERY SYSTEMS

6.2.1 TRANSDERMAL PATCHES

6.2.2 WEARABLE PATCHES

6.3 NASAL & PULMONARY DRUG DELIVERY SYSTEMS

6.3.1 NEBULIZERS

6.3.1.1 JET NEBULIZERS

6.3.1.2 MESH NEBULIZERS

6.3.1.3 ULTRASONIC NEBULIZER

6.3.2 EMPTY INHALER

6.3.2.1 METERED-DOSE INHALERS

6.3.2.2 DRY POWDER INHALERS

6.3.2.3 SOFT MIST INHALERS

6.3.3 STEAMERS

6.3.4 NASAL SPRAYS

6.4 DROP BOTTLES DRUG DELIVERY SYSTEMS

6.4.1 OCULAR DROP BOTTLES

6.4.2 NASAL DROP BOTTLES

6.4.3 COCHLEAR DROP BOTTLES

6.5 IMPLANTABLE DRUG DELIVERY DEVICES

6.5.1 INSERTS

6.5.2 DRUG ELUTING STENTS

6.5.3 PUMPS

7. GLOBAL DRUG DELIVERY DEVICES MARKET, BY TARGET APPLICATION (2023-2030, USD MILLION)

7.1 CARDIOVASCULAR DEVICES

7.2 DIABETES DEVICES

7.3 ONCOLOGY

7.4 INFECTIOUS DISEASES

7.5 OPHTHALMOLOGY DEVICES

7.6 RESPIRATORY DEVICES

7.7 AUTOIMMUNE DISEASES

7.8 CENTRAL NERVOUS SYSTEM DISORDERS

8. GLOBAL DRUG DELIVERY DEVICES MARKET, BY REGION (2023-2030, USD MILLION)

8.1 NORTH AMERICA

8.1.1 US

8.1.2 CANADA

8.2 EUROPE

8.2.1 GERMANY

8.2.2 FRANCE

8.2.3 SPAIN

8.2.4 ITALY

8.2.5 UK

8.2.6 REST OF THE EUROPE

8.3 ASIA PACIFIC

8.3.1 CHINA

8.3.2 JAPAN

8.3.3 INDIA

8.3.4 AUSTRALIA AND NEW ZEALAND

8.3.5 SOUTH KOREA

8.3.6 REST OF THE ASIA PACIFIC

8.4 MIDDLE EAST AND AFRICA

8.5 LATIN AMERICA

9. COMPETITIVE ANALYSIS

9.1 KEY PLAYERS FOOTPRINT ANALYSIS

9.2 MARKET SHARE ANALYSIS

9.3 KEY BRAND ANALYSIS

9.4 REGIONAL SNAPSHOT OF KEY PLAYERS

9.5 R&D EXPENDITURE OF KEY PLAYERS

10. COMPANY PROFILES2

10.1 KONINKLIJKE PHILIPS

10.1.1 BUSINESS OVERVIEW

10.1.2 PRODUCT PORTFOLIO

10.1.3 FINANCIAL SNAPSHOT3

10.1.4 RECENT DEVELOPMENTS

10.1.5 SWOT ANALYSIS

10.2 BECTON DICKINSON AND COMPANY

10.3 NOVARTIS AG,

10.4 GERRESHEIMER AG,

10.5 GEMINI PHARMACEUTICALS

10.6 RESYCA GMBH

10.7 LIFELONG MEDITECH PVT LTD

10.8 RECIPHARM AB

10.9 BRIGHT PHARMA CAPS

10.10 APTAR GROUP INC

10.11 ECLAM MEDICAL ACS LTD

10.12 YPSOMED HOLDING AG

10.13 NEMERA GROUP

10.14 OWEN MUMFORD LTD

10.15 HASELMEIER GMBH

10.16 SHL MEDICAL AG

11. APPENDIX

11.1 INDUSTRY SPEAK

11.2 QUESTIONNAIRE

11.3 AVAILABLE CUSTOM WORK

11.4 ADJACENT STUDIES

11.5 AUTHORS

12. REFERENCES

Key Notes: