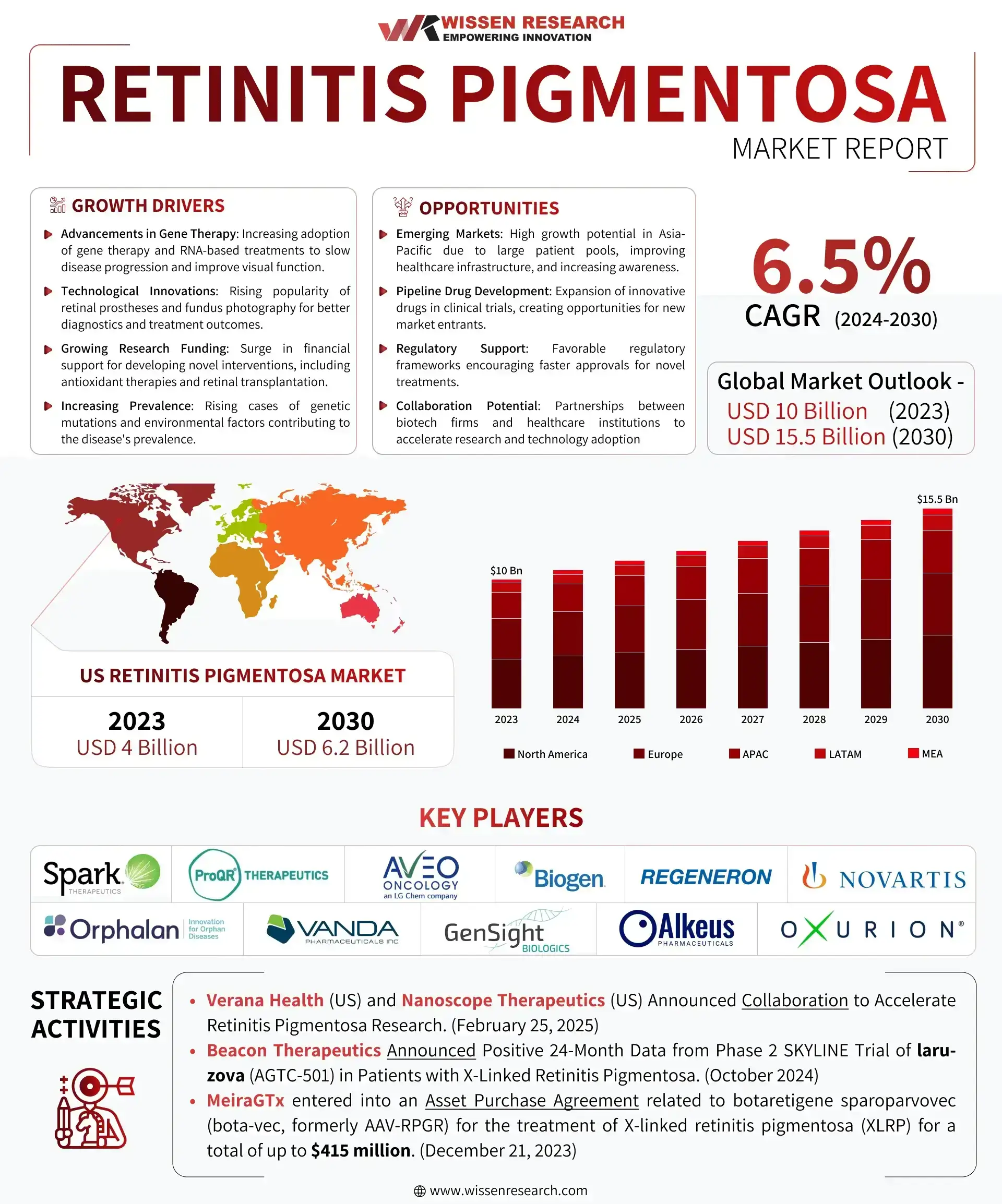

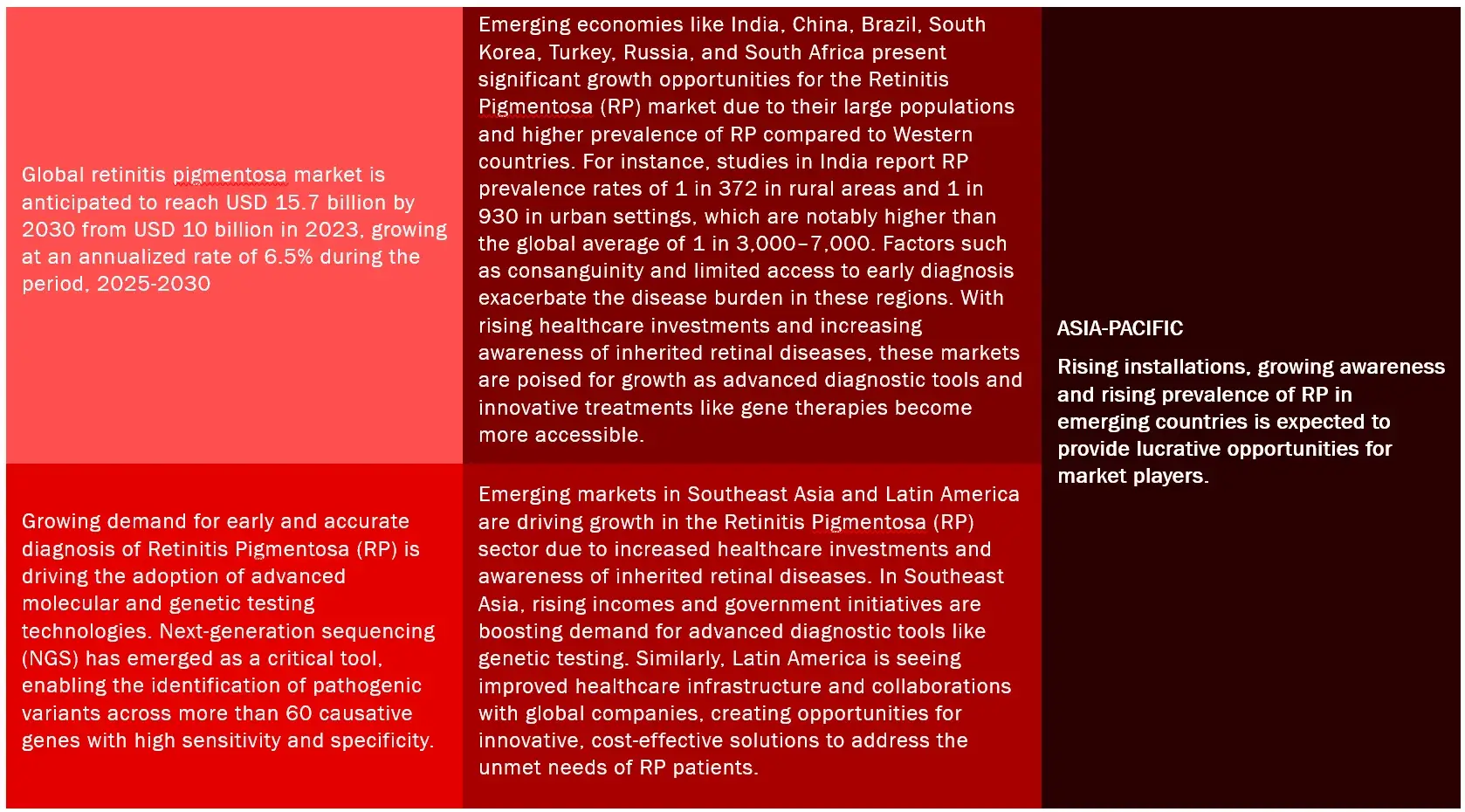

Wissen Research analyses that the global retinitis pigmentosa market is estimated at USD 10 billion in 2023 and is projected to reach USD 15.5 billion by 2030, expected to grow at a CAGR of 6.5% during the forecast period, 2024-2030.

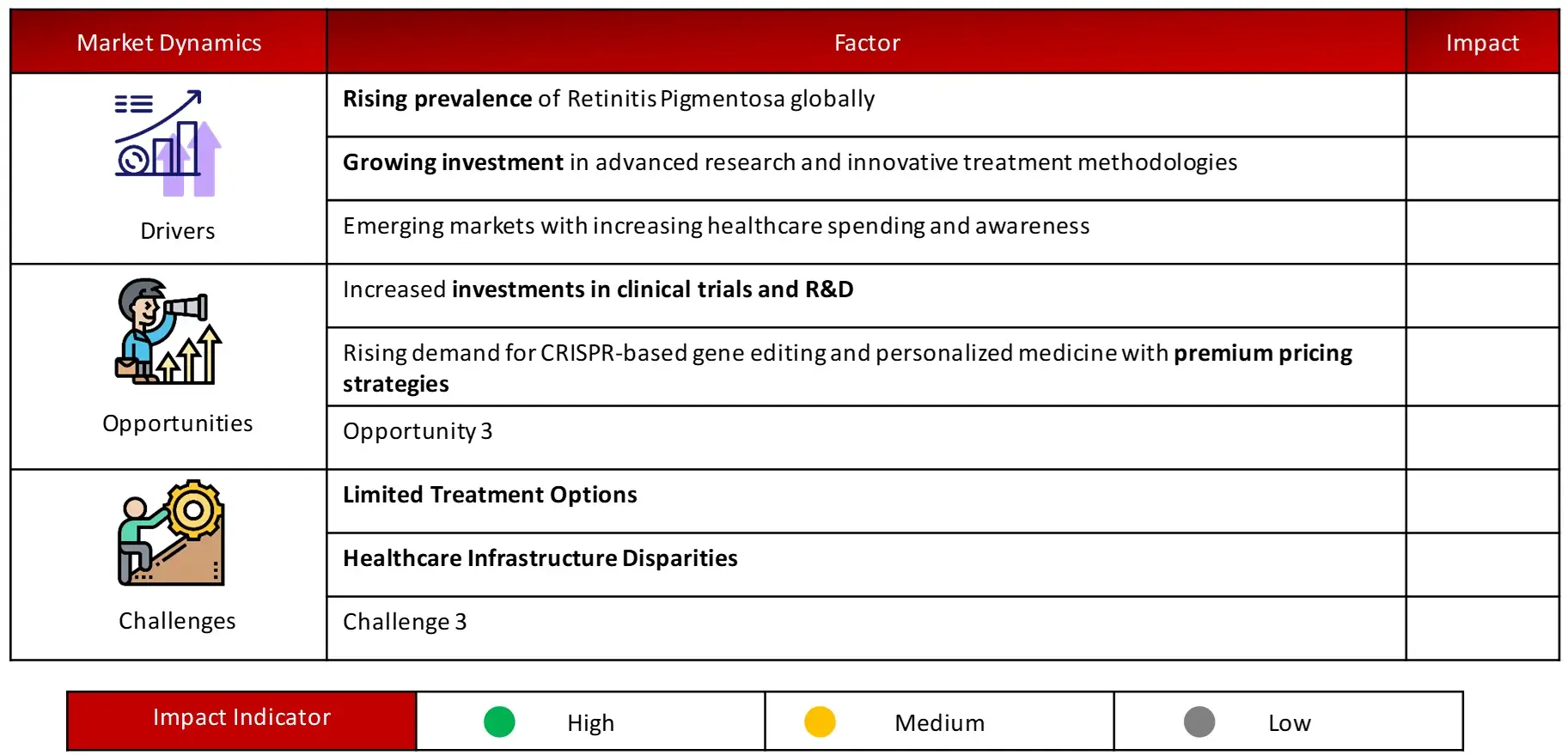

Key driving factors of Retinitis Pigmentosa market include rising prevalence, growing investment in advanced research and innovative treatment methodologies and emerging markets with increasing healthcare spending and awareness.

Challenges in the multiple sclerosis domain include limited treatment options and healthcare infrastructure disparities.

Pharmacological Therapies (supplements and anti-oxidants) have held the largest share in the market since 2022, with North America dominating the regional market share.

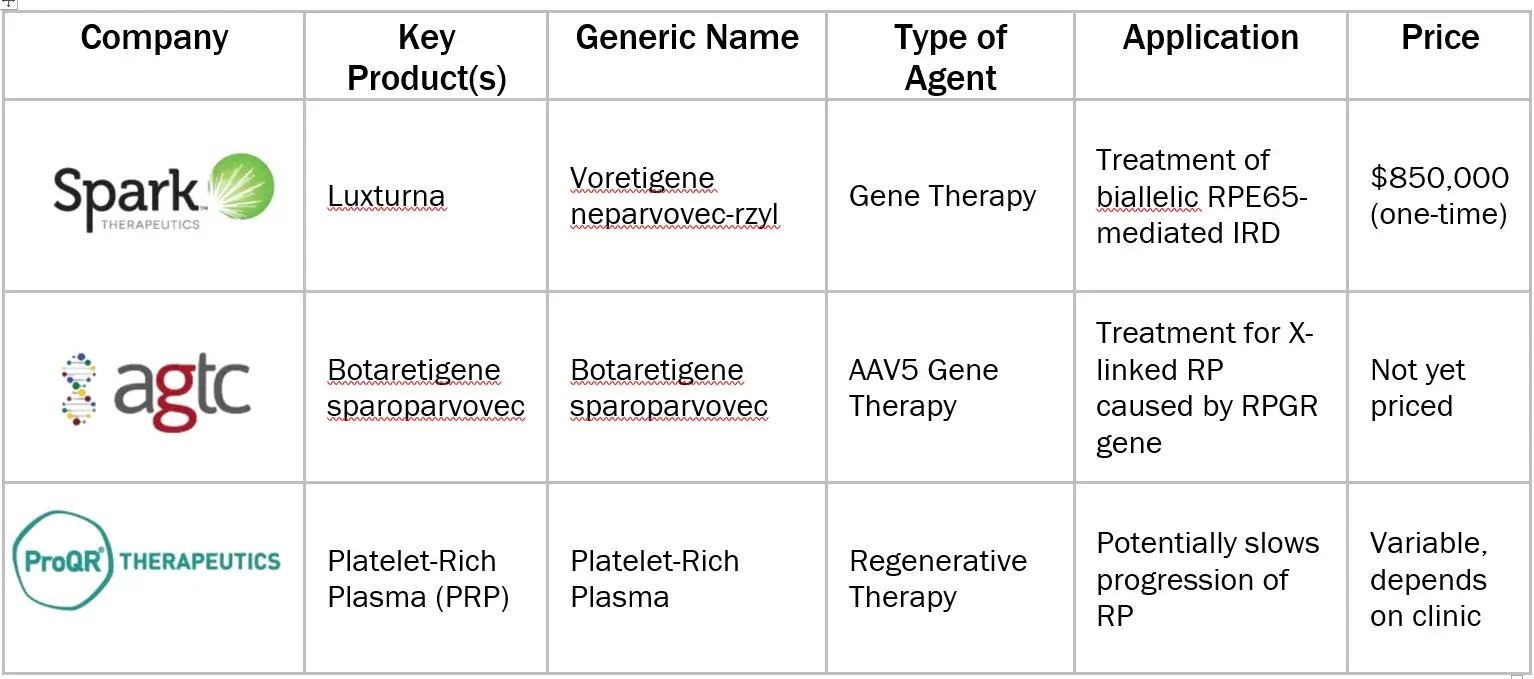

Key players functioning in retinitis pigmentosa sector are Spark Therapeutics, Inc., Proqr Therapeutics N.V., Gensight Biologics, Biogen Inc., Regeneron Pharmaceuticals, Inc., Novartis AG, among others

Further, the US with USD 4 billion market in 2024, holds majority share in the global retinitis pigmentosa market and is likely to remain the leading region growing a CAGR of 6.5% within this market, during the forecast period.

Drivers: Rising prevalence of Retinitis Pigmentosa globally

Retinitis pigmentosa (RP) has a global prevalence estimated at 1 in 3,000 to 1 in 5,000 individuals, affecting more than 1.5 million people worldwide, according to National Institutes of Health (NIH). The rising prevalence is driving market growth by increasing the demand for effective treatments and diagnostic tools. As genetic testing becomes more accessible, more cases are being identified, prompting investment in research and development for innovative therapies like gene therapy and retinal implants. Additionally, heightened awareness and the economic burden of vision loss associated with RP are pushing healthcare systems to prioritize solutions, further expanding the market.

Opportunities: Rising demand for CRISPR-based gene editing and personalized medicine with premium pricing strategies in Retinitis Pigmentosa Market

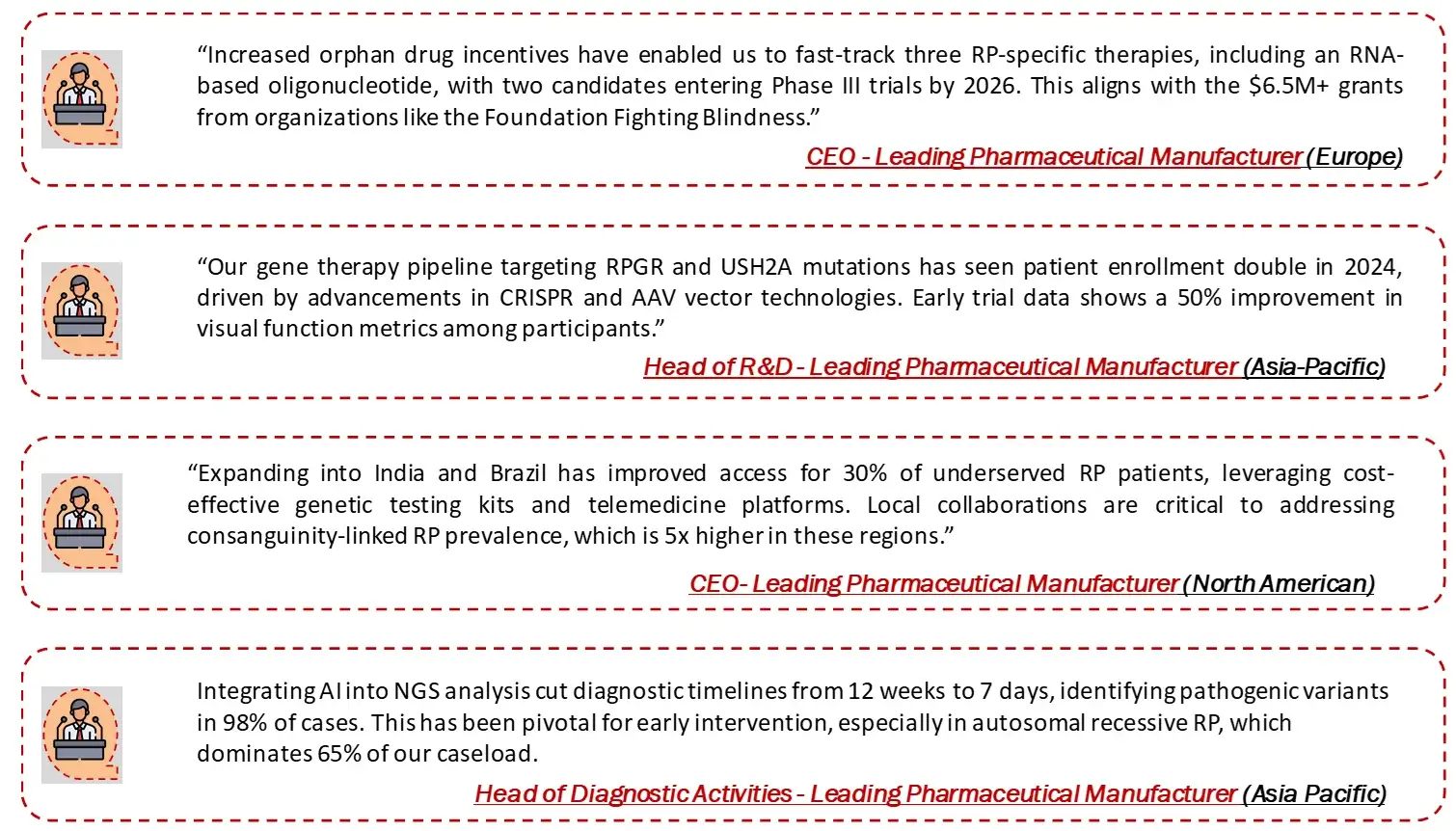

The rising demand for CRISPR-based gene editing and personalized medicine in the Retinitis Pigmentosa (RP) market is driven by its ability to precisely target genetic mutations causing RP, enabling tailored therapies with premium pricing potential. For instance, Intellia Therapeutics partnered with SparingVision to develop CRISPR-based ocular therapies, while the Foundation Fighting Blindness has invested $6.5 million in research for inherited retinal diseases, including CRISPR applications. Such collaborations and funding efforts highlight the growing interest in leveraging cutting-edge technologies to revolutionize RP treatment and improve patient outcomes.

Challenges: Healthcare Infrastructure Disparities in Retinitis Pigmentosa Market

Healthcare infrastructure disparities significantly challenge the Retinitis Pigmentosa (RP) market by limiting access to essential diagnostic and treatment services. In many regions, especially in low-income countries, inadequate healthcare facilities and a shortage of trained professionals hinder timely diagnosis and effective management of RP. For example, in rural India, the prevalence of RP is notably high due to factors like consanguineous marriages, yet access to specialized care and genetic counseling remains limited. This disparity not only affects patient outcomes but also exacerbates the social and economic burden on families, as they struggle with the implications of vision loss. Moreover, the financial strain on healthcare systems from untreated RP cases highlights the urgent need for investment in healthcare infrastructure to ensure equitable access to innovative therapies and support services for all patients.

The retinitis pigmentosa market report offers information on the latest advancements in the industry, as well as product portfolio analysis, supply chain/value chain analysis, market share, and the effects of localized and domestic players. It also analyses potential revenue opportunities and changes in market regulations, as well as market size, category market growth, application dominance, product approvals, product launches, geographic expansions, and technological innovations. For an analyst brief and other information on the retinitis pigmentosa market, get in touch with Wissen Research. Our staff can assist you in making well-informed decisions that will lead to market expansion.

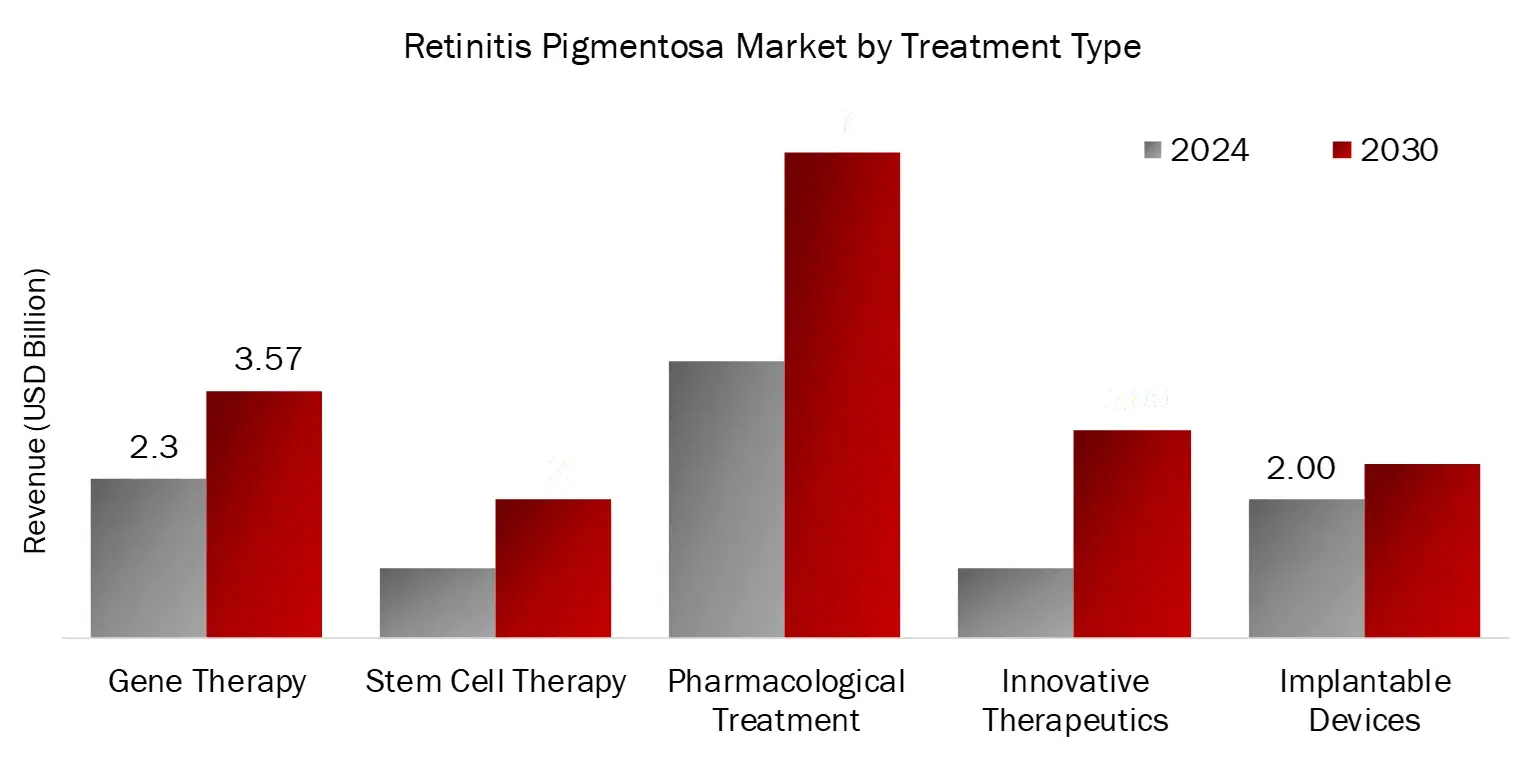

Pharmacological Therapies Segment Dominated the Retinitis Pigmentosa Market by Treatment Type in 2023

The pharmacological therapies segment dominated the Retinitis Pigmentosa (RP) market by treatment type in 2023 due to a combination of factors, including the limited availability of approved treatments, with LUXTURNA being the only gene therapy specifically for patients with RPE65 mutations. As most RP patients rely on best supportive care, such as vitamin supplements and visual aids, pharmacological interventions formed a significant portion of the market. Additionally, ongoing research and advancements in the clinical pipeline, including novel therapies targeting specific genetic mutations like Ultevursen for the USH2A gene, have bolstered this segment.

The pharmacological therapies segment dominated the Retinitis Pigmentosa (RP) market by treatment type in 2023 due to a combination of factors, including the limited availability of approved treatments, with LUXTURNA being the only gene therapy specifically for patients with RPE65 mutations. As most RP patients rely on best supportive care, such as vitamin supplements and visual aids, pharmacological interventions formed a significant portion of the market. Additionally, ongoing research and advancements in the clinical pipeline, including novel therapies targeting specific genetic mutations like Ultevursen for the USH2A gene, have bolstered this segment.

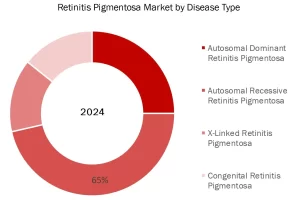

Autosomal Recessive RP held the largest market share in 2023, accounting for a significant 65% market share.

Autosomal recessive Retinitis Pigmentosa (RP) held the largest market share in 2023, accounting for 65%, due to its higher prevalence compared to other inheritance patterns and the significant advancements in identifying causative genetic mutations. Mutations in genes like USH2A, responsible for 10–15% of autosomal recessive RP cases, have driven research and development of targeted therapies. Additionally, the autosomal recessive inheritance pattern, which requires two copies of a mutated gene from both parents, is more common in populations with consanguineous marriages, further contributing to its dominance. This segment’s growth is also supported by increasing genetic testing capabilities, enabling better diagnosis and therapeutic interventions for affected individuals.

Autosomal recessive Retinitis Pigmentosa (RP) held the largest market share in 2023, accounting for 65%, due to its higher prevalence compared to other inheritance patterns and the significant advancements in identifying causative genetic mutations. Mutations in genes like USH2A, responsible for 10–15% of autosomal recessive RP cases, have driven research and development of targeted therapies. Additionally, the autosomal recessive inheritance pattern, which requires two copies of a mutated gene from both parents, is more common in populations with consanguineous marriages, further contributing to its dominance. This segment’s growth is also supported by increasing genetic testing capabilities, enabling better diagnosis and therapeutic interventions for affected individuals.

North America held the largest market share in Retinitis Pigmentosa Market in the forecast period

Retinitis Pigmentosa market analysis encompassed a detailed evaluation of five key regions: North America, Europe, Asia-Pacific, Middle East & Africa, and Latin America. These regions were assessed based on healthcare infrastructure, regulatory frameworks, technological advancements, and market trends. North America held the largest market share in the Retinitis Pigmentosa (RP) market during the forecast period, primarily due to its well-established healthcare infrastructure, high levels of awareness about retinal diseases, and significant investment in research and development. In 2022, this region accounted for a substantial portion of the market, driven by the presence of major pharmaceutical companies and advanced diagnostic technologies. The United States, in particular, has a high prevalence of retinal disorders, which has led to increased demand for effective treatments and diagnostic services. Additionally, favorable reimbursement policies and a growing focus on innovative treatment methods further bolster the market’s growth in North America, positioning it as a leader in the global RP landscape.

Major players operating in Retinitis Pigmentosa market are:

BRAND ANALYSIS: RETINITIS PIGMENTOSA MARKET

Sources: Secondary Research

Sources: Secondary ResearchPRIMARY INSIGHTS FROM KEY OPINION LEADERS

Particulars | Details |

Report | Retinitis Pigmentosa Market |

Forecast Period | 2024-2030 |

Base Year | 2023 |

Format | |

Estimated Market Size (2023) | USD 10 Billion |

CAGR (2024-2030) | 6.5% |

Number of Pages | 170 |

Number of Tables | 161 |

Number of Figures | 33 |

Key Segments | Retinitis Pigmentosa Market Treatment Outlook (Gene Therapy, Cell Therapy, Pharmacological Treatment, Innovative Therapeutics, Implantable Devices)

Retinitis Pigmentosa Market Disease Outlook (Autosomal Dominant Retinitis Pigmentosa, Autosomal Recessive Retinitis Pigmentosa, X-Linked Retinitis Pigmentosa, Congenital Retinitis Pigmentosa) Retinitis Pigmentosa Market Patient Demographic Outlook (Retinitis Pigmentosa Treatment Market by, Age Group, Retinitis Pigmentosa Treatment Market by, Gender) Retinitis Pigmentosa Market End User Outlook (Hospitals and Clinics, Specialized Eye Care Centers, Home Care and Ambulatory Care Centers, Research Institutes and Biotechnology Companies) |

Regions Covered | North America: US and Canada Europe: Germany, UK, France, Italy, Spain, and Rest of the Europe Asia-Pacific: China, Japan, India, South Korea, Australia and New Zealand, and Rest of the Asia-Pacific Latin America Middle East and Africa |

Key Players Covered (Majority Share Holders) | Spark Therapeutics, Inc. (US), Proqr Therapeutics N.V. (Netherlands), Gensight Biologics (France), Biogen Inc. (US) , Regeneron Pharmaceuticals, Inc. (US), Novartis AG (Switzerland), Orphalan SA (France), Aveo Pharmaceuticals, Inc. (US) , Vanda Pharmaceuticals Inc. (US), Oxurion NV (Belgium), Alkeus Pharmaceuticals, Inc. (US) |

Introduction

MARKET DEFINITION

The Retinitis Pigmentosa (RP) Treatment Market refers to the global market for medical products and therapies designed to treat Retinitis Pigmentosa, a group of rare genetic disorders that cause progressive degeneration of the retina, leading to vision impairment and, in some cases, blindness.

FIGURE: RETINITIS PIGMENTOSA MARKET SEGMENTS

Sources: Company Websites and Wissen Research Analysis

Sources: Company Websites and Wissen Research Analysis

FIGURE: YEARS FRAMEWORK CONSIDERED IN THE STUDY

Sources: Wissen Research Analysis

Sources: Wissen Research Analysis

Key Stakeholders

Key objectives of the Study

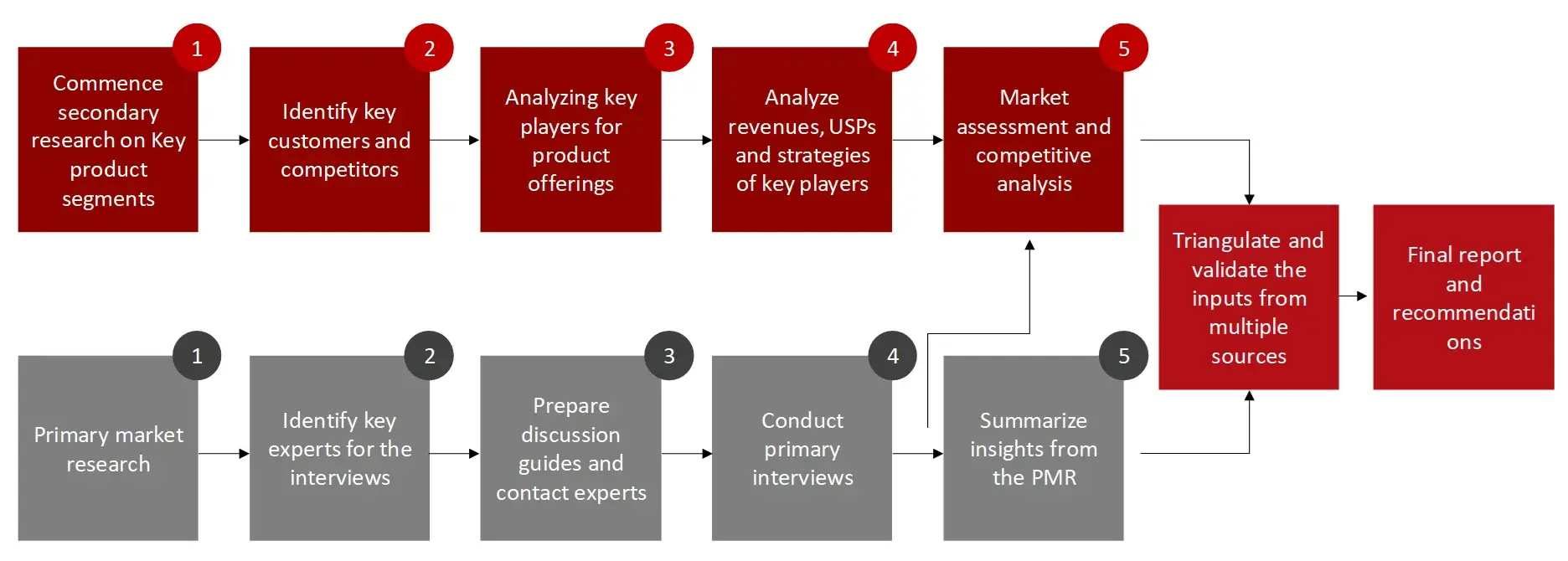

Research Methodology

The aim of the study is to examine the key market forces such as drivers, opportunities, restraints, challenges, and strategies impacting the market ecosystem. To monitor company advancements such as patents granted, product launches, expansions, and collaborations of key players, analysing their competitive landscape based on various parameters of business and product strategy. Markey sizing will be estimated using top-down and bottom-up approaches. Using market breakdown and data triangulation techniques, market sizing of segments and sub-segments will be estimated.

FIGURE: RESEARCH DESIGN

Sources: Wissen Research Analysis

Sources: Wissen Research Analysis

Research Approach

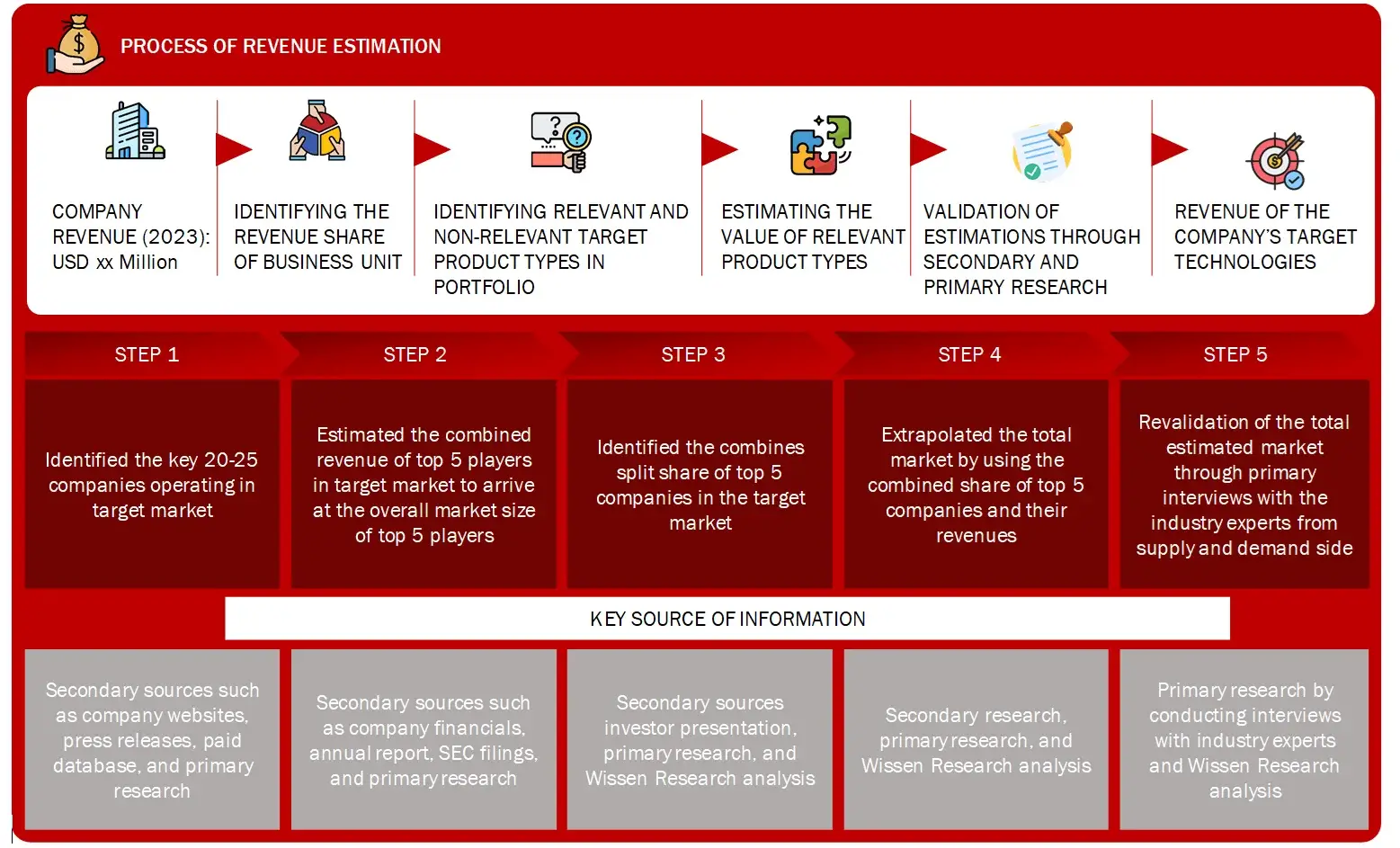

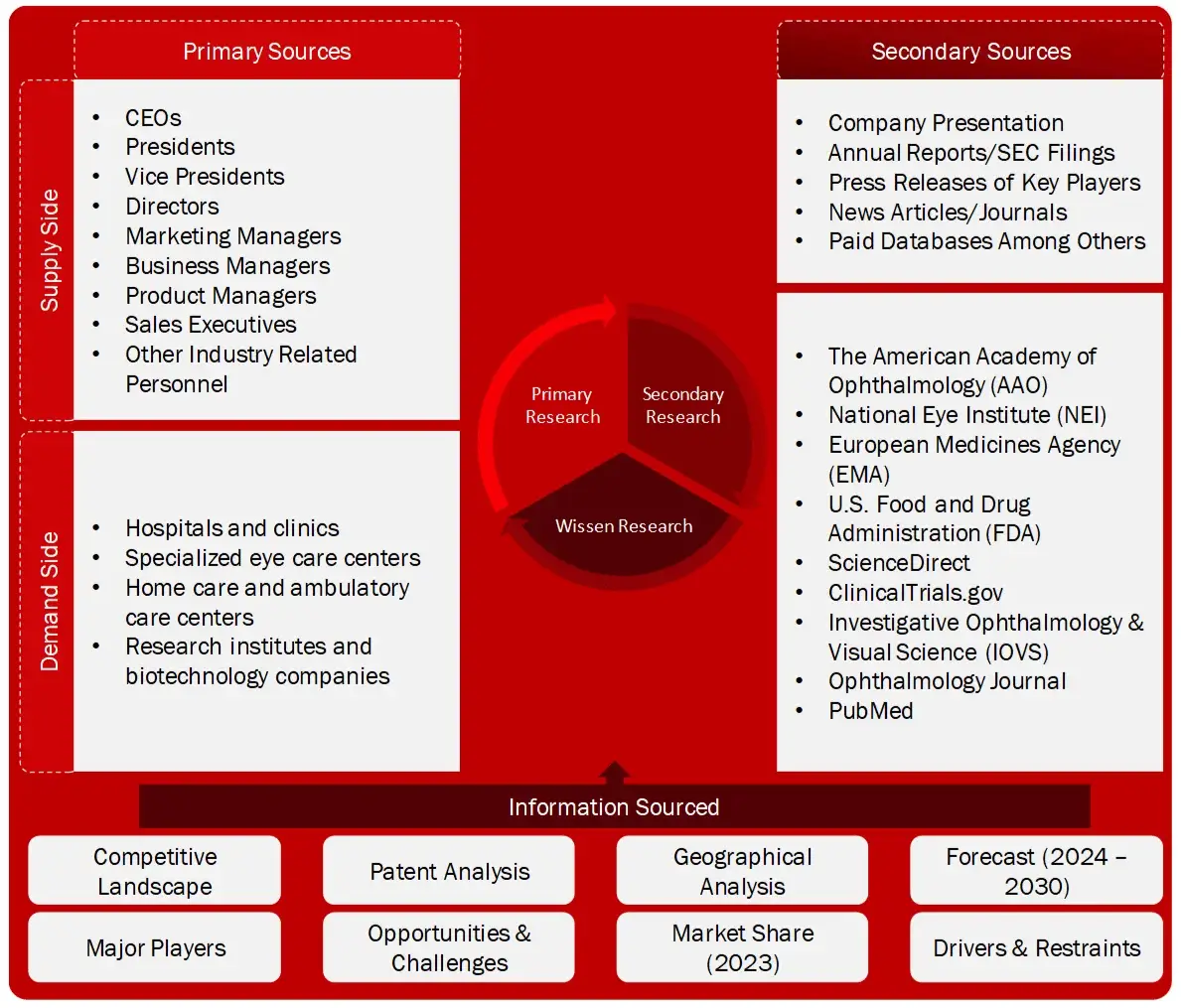

Collecting Secondary Data

The process of collating secondary research data involves the utilization of databases, secondary sources, annual reports, investor presentations, directories, and SEC filings of companies. Secondary research will be utilized to identify and gather information beneficial for the in-depth, technical, market-oriented, and commercial analysis of the retinitis pigmentosa treatment market. A database of the key industry leaders will also be compiled using secondary research.

Collecting Primary Data

The primary research data will be conducted after acquiring knowledge about the retinitis pigmentosa treatment market scenario through secondary research. A significant number of primary interviews will be conducted with stakeholders from both the demand and supply side (including various industry experts, such as Vice Presidents (VPs), Chief X Officers (CXOs), Directors from business development, marketing and product development teams, product manufacturers) across major countries within Europe, Asia Pacific, North America, Latin America, and Middle East. Primary data for this report will be collected through questionnaires, emails, and telephonic interviews.

FIGURE: BREAKDOWN OF PRIMARY INTERVIEWS FROM SUPPLY SIDE

FIGURE: BREAKDOWN OF PRIMARY INTERVIEWS FROM DEMAND SIDE

FIGURE: PROPOSED PRIMARY PARTICIPANTS FROM DEMAND AND SUPPLY SIDE

Note: Above mentioned companies are non- exhaustive

Market Size Estimation

All major manufacturers offering various multiple sclerosis will be identified at the global/regional level. Revenue mapping will be done for the major players, which will further be extrapolated to arrive at the global market value of each type of segment. The market value of multiple sclerosis market will also split into various segments and sub segments at the region level based on:

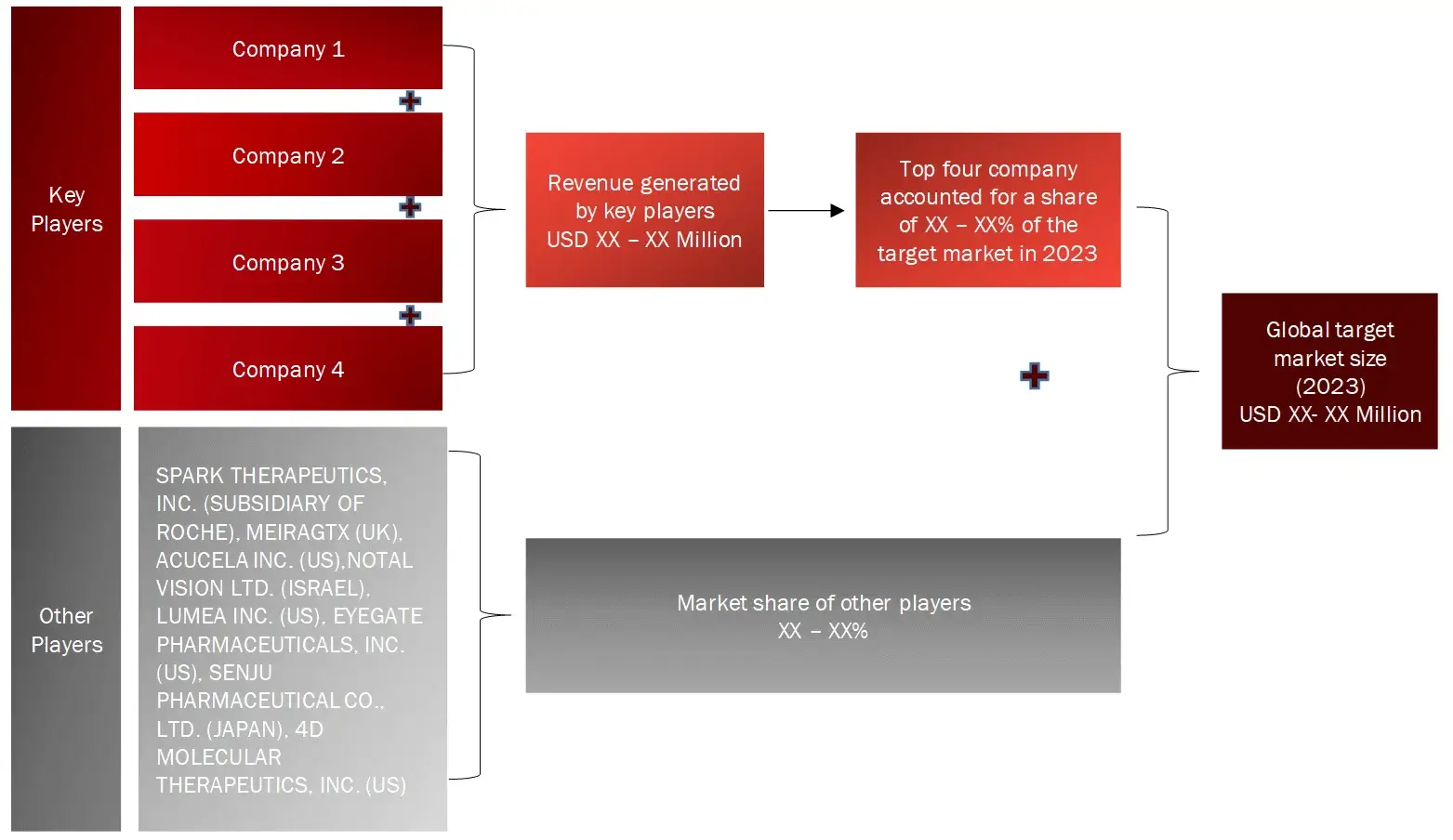

FIGURE: REVENUE MAPPING BY COMPANY (ILLUSTRATION)

Sources: Company Websites, Annual Reports, SEC Filings, Press Releases, Investor Presentation, Paid Database, and Wissen Research Analysis.

Sources: Company Websites, Annual Reports, SEC Filings, Press Releases, Investor Presentation, Paid Database, and Wissen Research Analysis.

FIGURE: REVENUE SHARE ANALYSIS OF KEY PLAYERS (SUPPLY SIDE)

Sources: Company Websites, Annual Reports, SEC Filings, Press Releases, Investor Presentation, Paid Database, and Wissen Research Analysis.

Sources: Company Websites, Annual Reports, SEC Filings, Press Releases, Investor Presentation, Paid Database, and Wissen Research Analysis.

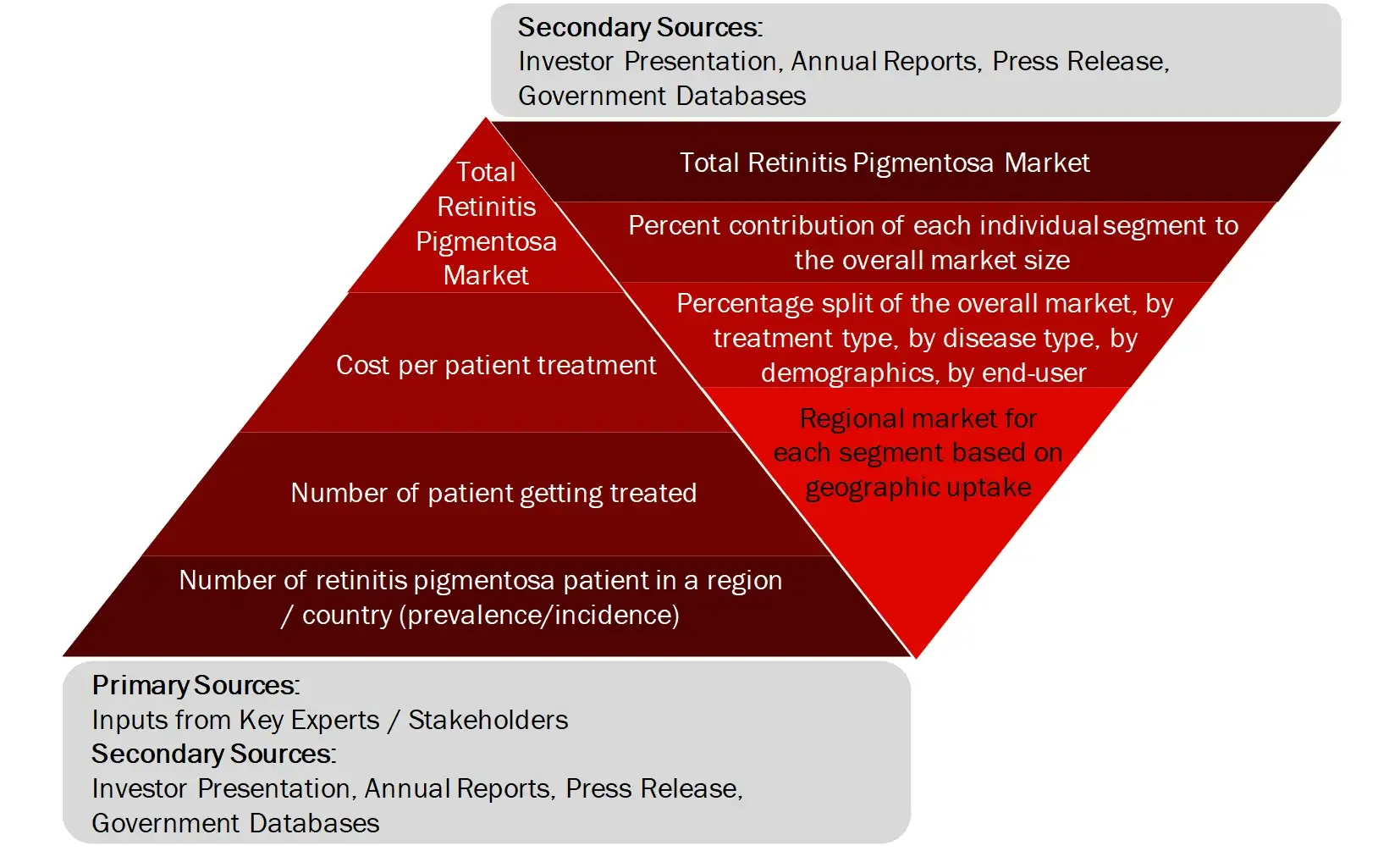

FIGURE: MARKET SIZE ESTIMATION TOP-DOWN AND BOTTOM-UP APPROACH

Sources: Company Websites, Annual Reports, SEC Filings, Press Releases, Investor Presentation, Paid Database, and Wissen Research Analysis.

Sources: Company Websites, Annual Reports, SEC Filings, Press Releases, Investor Presentation, Paid Database, and Wissen Research Analysis.

FIGURE: ANALYSIS OF DROCS FOR GROWTH FORECAST

Sources: The American Academy of Ophthalmology (AAO), National Eye Institute (NEI), European Medicines Agency (EMA), U.S. Food and Drug Administration (FDA), ScienceDirect, ClinicalTrials.gov, Investigative Ophthalmology & Visual Science (IOVS), Ophthalmology Journal, PubMed, Company Presentation, Annual Reports/SEC Filings, Press Releases of Key Players, News Articles/Journals, Primary Market Research, and Paid Databases Among Others

Sources: The American Academy of Ophthalmology (AAO), National Eye Institute (NEI), European Medicines Agency (EMA), U.S. Food and Drug Administration (FDA), ScienceDirect, ClinicalTrials.gov, Investigative Ophthalmology & Visual Science (IOVS), Ophthalmology Journal, PubMed, Company Presentation, Annual Reports/SEC Filings, Press Releases of Key Players, News Articles/Journals, Primary Market Research, and Paid Databases Among Others

FIGURE: GROWTH FORECAST ANALYSIS UTILIZING MULTIPLE PARAMETERS

Sources: Company Websites, Annual Reports, SEC Filings, Press Releases, Investor Presentation, Paid Database, and Wissen Research Analysis.

Sources: Company Websites, Annual Reports, SEC Filings, Press Releases, Investor Presentation, Paid Database, and Wissen Research Analysis.

Research Design

After arriving at the overall market size-using the market size estimation processes-the market will be split into several segments and sub segment. To complete the overall market engineering process and arrive at the exact statistics of each market segment and sub segment, the data triangulation, and market breakdown procedures will be employed, wherever applicable. The data will be triangulated by studying various factors and trends from both the demand and supply sides in the multiple sclerosis market industry.

Sources: The American Academy of Ophthalmology (AAO), National Eye Institute (NEI), European Medicines Agency (EMA), U.S. Food and Drug Administration (FDA), ScienceDirect, ClinicalTrials.gov, Investigative Ophthalmology & Visual Science (IOVS), Ophthalmology Journal, PubMed, Company Presentation, Annual Reports/SEC Filings, Press Releases of Key Players, News Articles/Journals, Primary Market Research, and Paid Databases Among Others

Sources: The American Academy of Ophthalmology (AAO), National Eye Institute (NEI), European Medicines Agency (EMA), U.S. Food and Drug Administration (FDA), ScienceDirect, ClinicalTrials.gov, Investigative Ophthalmology & Visual Science (IOVS), Ophthalmology Journal, PubMed, Company Presentation, Annual Reports/SEC Filings, Press Releases of Key Players, News Articles/Journals, Primary Market Research, and Paid Databases Among Others

1.1 KEY OBJECTIVES

1.2 DEFINITIONS

1.2.1 IN SCOPE

1.2.2 OUT OF SCOPE

1.3 SCOPE OF THE REPORT

1.4 SCOPE RELATED LIMITATIONS

1.5 KEY STAKEHOLDERS

2. RESEARCH METHODOLOGY

2.1 RESEARCH APPROACH

2.2 RESEARCH METHODOLOGY / DESIGN

2.3 MARKET SIZE ESTIMATION APPROACHES

2.3.1 SECONDARY RESEARCH

2.3.2 PRIMARY RESEARCH

2.3.2.1 KEY INSIGHTS FROM INDUSTRY EXPERTS

2.4 DATA VALIDATION & TRIANGULATION

2.5 ASSUMPTIONS OF THE STUDY

3. EXECUTIVE SUMMARY & PREMIUM CONTENT

3.1 GLOBAL MARKET OUTLOOK

3.2 KEY MARKET FINDINGS

4. MARKET OVERVIEW

4.1 RETINITIS PIGMENTOSA: DISEASE OVERVIEW

4.1.1 INTRODUCTION

4.1.2 SIGNS AND SYMPTOMS

4.1.3 CAUSES OF RETINITIS PIGMENTOSA

4.1.4 CLASSIFICATION OF RETINITIS PIGMENTOSA

4.1.5 PATHOPHYSIOLOGY

4.1.6 DIAGNOSIS OF RETINITIS PIGMENTOSA

4.1.6.1 DIAGNOSTIC TESTS

4.1.6.2. DIFFERENTIAL DIAGNOSIS OF RETINITIS PIGMENTOSA

4.1.6.3 DIAGNOSTIC GUIDELINES

4.1.7 PROGNOSIS

4.1.8 TREATMENT OF RETINITIS PIGMENTOSA

4.1.8.1 FUTURE TREATMENT MODALITIES

4.1.8.2 GENERAL RECOMMENDATIONS FOR RETINITIS PIGMENTOSA TREATMENT

4.1.8.3 TREATMENT GUIDELINES FOR RETINITIS PIGMENTOSA

4.2 MARKET DYNAMICS

4.2.1 MARKET DRIVERS

4.2.2MARKET OPPORTUNITIES

4.2.3 RESTRAINTS/CHALLENGES

4.3 END USER PERCEPTION

4.4 NEED GAP ANALYSIS

4.5 KEY CONFERENCES

4.6 EPIDEMIOLOGY

4.7 PATIENT JOURNEY MAPPING: RETINITIS PIGMENTOSA

4.8 SUPPLY CHAIN / VALUE CHAIN ANALYSIS

4.9 INDUSTRY TRENDS

4.10 PORTER’S FIVE FORCES ANALYSIS

4.11 REGULATORY LANDSCAPE

4.11.1 NORTH AMERICA

4.11.2 EUROPE

4.11.3 ASIA PACIFIC

4.12 REIMBURSEMENT SCENARIO

5. PATENT ANALYSIS

5.1 TOP ASSIGNEES

5.2 GEOGRAPHY FOCUS OF TOP ASSIGNEES

5.3 LEGAL STATUS

5.4 TECHNOLOGY EVOLUTION

5.5 KEY PATENTS

5.6 PATENT TRENDS AND INNOVATIONS

6. LINICAL TRIAL ANALYSIS

6.1 ANALYSIS BY TRIAL REGISTRATION YEAR

6.2 ANALYSIS BY PHASE OF DEVELOPMENT

6.3 ANALYSIS BY TRIAL STATUS

6.4 ANALYSIS BY NUMBER OF PATIENTS ENROLLED

6.5 ANALYSIS BY STUDY DESIGN

6.6 ANALYSIS BY TYPE OF THERAPY / DRUG

6.7 ANALYSIS BY GEOGRAPHY

6.8 ANALYSIS BY KEY SPONSORS / COLLABORATORS

7. GLOBAL RETINITIS PIGMENTOSA TREATMENT MARKET BY, TREATMENT TYPE (2023-2030, USD MILLION)

7.1 GENE THERAPY

7.1.1 GENE EDITING

7.1.2 GENE REPLACEMENT THERAPY

7.2 STEM CELL THERAPY

7.2.1 RETINA REGENERATION

7.2.2 STEM CELL LINES

7.3 PHARMACOLOGICAL TREATMENT

7.3.1 RETINOID-BASED DRUGS

7.3.2 ANTIOXIDANTS AND SUPPLEMENTS

7.4 INNOVATIVE THERAPEUTICS

7.5 IMPLANTABLE DEVICES

7.5.1 RETINAL IMPLANTS

7.5.2 RETINAL PROSTHESES

8. GLOBAL RETINITIS PIGMENTOSA TREATMENT MARKET BY, DISEASE TYPE / MUTATION (2023-2030, USD MILLION)

8.1 AUTOSOMAL DOMINANT RETINITIS PIGMENTOSA

8.2 AUTOSOMAL RECESSIVE RETINITIS PIGMENTOSA

8.3 X-LINKED RETINITIS PIGMENTOSA

8.4 CONGENITAL RETINITIS PIGMENTOSA

9. GLOBAL RETINITIS PIGMENTOSA TREATMENT MARKET BY, PATIENT DEMOGRAPHICS (2023-2030, USD MILLION)

9.1 RETINITIS PIGMENTOSA TREATMENT MARKET BY, AGE GROUP

9.1.1 PEDIATRIC PATIENTS

9.1.2 ADULTS

9.1.3 ELDERLY PATIENTS

9.2 RETINITIS PIGMENTOSA TREATMENT MARKET BY, GENDER

9.2.1 MALE PATIENTS

9.2.2 FEMALE PATIENTS

10. GLOBAL RETINITIS PIGMENTOSA TREATMENT MARKET BY, END-USER (2023-2030, USD MILLION)

10.1 HOSPITALS AND CLINICS

10.2 SPECIALIZED EYE CARE CENTERS

10.3 HOME CARE AND AMBULATORY CARE CENTERS

10.4 RESEARCH INSTITUTES AND BIOTECHNOLOGY COMPANIES

11. GLOBAL PHARMACEUTICAL CDMO MARKET BY, REGION (2023-2030, USD MILLION)

11.1 NORTH AMERICA

11.1.1 US

11.1.2 CANADA

11.2 EUROPE

11.2.1 GERMANY

11.2.2. FRANCE

11.2.3 SPAIN

11.2.4 ITALY

11.2.5 UK

11.2.6 REST OF THE EUROPE

11.3 ASIA-PACIFIC

11.3.1 CHINA

11.3.2 JAPAN

11.3.3 INDIA

11.3.4 AUSTRALIA AND NEW ZEALAND

11.3.5 SOUTH KOREA

11.3.6 REST OF THE ASIA-PACIFIC

11.4 MIDDLE EAST AND AFRICA

11.5 LATIN AMERICA

12. COMPETITIVE ANALYSIS

12.1 PRODUCT PIPELINE: RETINITIS PIGMENTOSA TREATMENT

12.2 KEY PLAYERS FOOTPRINT ANALYSIS

12.3 MARKET SHARE ANALYSIS (2023/2024)

12.4 REGIONAL SNAPSHOT OF KEY PLAYERS

12.5 R&D EXPENDITURE OF KEY PLAYERS

13. COMPANY PROFILES

13.1 SPARK THERAPEUTICS, INC. (SUBSIDIARY OF ROCHE)

13.1.1 BUSINESS OVERVIEW

13.1.2 PRODUCT PORTFOLIO

13.1.3 FINANCIAL SNAPSHOT

13.1.4 RECENT DEVELOPMENTS

13.1.4.1 MERGER/ACQUISITIONS

13.1.4.2 PRODUCT APPROVAL/LAUNCHES

13.1.4.3 PARTNERSHIP/COLLABORATIONS/AGREEMENTS

13.1.4.4 EXPANSIONS

13.2 PROQR THERAPEUTICS N.V. (NETHERLANDS)

13.3 GENSIGHT BIOLOGICS (FRANCE)

13.4 BIOGEN INC. (US)

13.5 REGENERON PHARMACEUTICALS, INC. (US)

13.6 NOVARTIS AG (SWITZERLAND)

13.7 ORPHALAN SA (FRANCE)

13.8 AVEO PHARMACEUTICALS, INC. (US)

13.9 VANDA PHARMACEUTICALS INC. (US)

13.10 HORAMA (FRANCE)

13.11 OXURION NV (BELGIUM)

13.12 ALKEUS PHARMACEUTICALS, INC. (US)

13.13 MEIRAGTX (UK)

13.14 ACUCELA INC. (US)

13.15 NOTAL VISION LTD. (ISRAEL)

13.16 LUMEA INC. (US)

13.17 EYEGATE PHARMACEUTICALS, INC. (US)

13.18 SENJU PHARMACEUTICAL CO., LTD. (JAPAN)

13.19 4D MOLECULAR THERAPEUTICS, INC. (US)

13.20 ASTELLAS PHARMA INC. (JAPAN)

13.21 CLINO CORPORATION (JAAN)

14. APPENDIX

14.1 INDUSTRY SPEAK

14.2 QUESTIONNAIRE/DISCUSSION GUIDE

14.3 AVAILABLE CUSTOM WORK

14.4 ADJACENT STUDIES

14.5 AUTHORS

REFERENCES

Key Notes:

Note 1 – Contents in the ToC / market segments are tentative and might change as the research proceeds.

Note 2 – List of companies is not exhaustive and might change during the course of study.

Note 3 – Details on key financials might not be captured in case of unlisted companies.

Note 4 – SWOT analysis will be provided for top 3-5 companies.